Geopolitics, inflation expectations, and the repricing of rate risk

Summary

Middle East tensions rippled through rates and FX, with oil-driven inflation concerns reversing the recent disinflation-led rally in swap rates. The shift makes expected central bank easing less straightforward and has strengthened the dollar’s safe-haven appeal.

Global rate markets and the impact of Middle East conflict

Recent events in the Middle East immediately rippled through global rate markets, leading to a sharp repricing across USD, EUR and GBP curves. While the conflict has implications across a wide range of areas, the focus for markets right now is oil — how far prices could move, and the transmission mechanism that feeds through into inflation and, ultimately, central bank policy.

Up until recently, swap rates had been drifting steadily lower since year-end, supported by growing confidence in disinflation and expectations of policy easing. That trend has reversed this week.

Analysis of 5-year swap rate movements

You can see the shift clearly in 5-year swap rates across SOFR, EUR and SONIA when comparing three points in time: the end of 2025, the week before the conflict began, and one week after it started.

| Date | 5-yr Swap Rates | ||

| SOFR | EURIBOR | SONIA | |

| December 31, 2025 | 3.46% | 2.57% | 3.65% |

| February 27, 2026 | 3.22% | 2.34% | 3.52% |

| March 6, 2026 | 3.45% | 2.67% | 3.97% |

Source: Chatham Financial

The shift in market narrative

By late February, 5-year swap rates had fallen meaningfully from year-end levels, reflecting growing confidence that central bank rate cuts would begin to filter through in 2026. Borrowers across currencies were considering locking in fixed rates on the assumption that what the forward curve was pricing in for rate cuts would come through in the following months.

However, in the space of a week, that narrative shifted. Between 27 February and 6 March, 5-year SOFR rose by more than 20 basis points, EUR swaps climbed more than 30 basis points, and SONIA moved nearly 45 basis points higher. In sterling markets in particular, the reversal has been striking, pushing SONIA swaps well above year-end levels.

Inflation concerns and central bank policy

The driver is renewed concern around inflation. Oil and broader commodity prices have moved higher in response to geopolitical tensions. Just as inflation seemed to be entering its final phase of moderation, renewed energy price pressure has introduced uncertainty around the path back to target.

For central banks - Bank of England, the Federal Reserve and the ECB, this complicates the policy outlook. Any renewed upside risk to inflation, or even to inflation expectations, makes it harder to deliver rate cuts as quickly as previously anticipated.

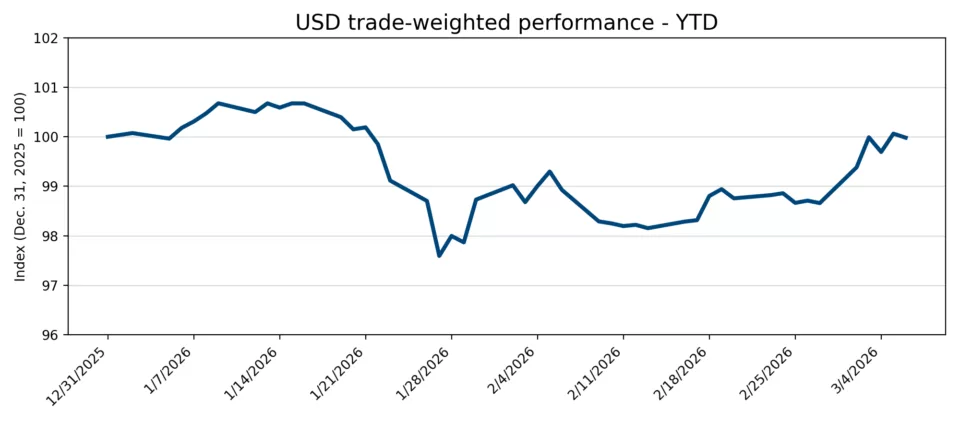

The US dollar as a safe-haven asset

At the same time, the US dollar has strengthened on its safe-haven status amid geopolitical uncertainty. As shown in the chart below, USD Trade-Weighted Index, indexed to 100 at 1 January 2026, the dollar’s early-year softness has given way to a more pronounced move higher in recent sessions, reflecting renewed demand for safe-haven assets. Proving, again, that concerns over debasement of USD were overblown, and in times of risk off, buying USD is considered the safest move.

Source: Bloomberg

For those exposed to continued USD weakness and had been caught out with the pace and extent of that move, there is now an opportunity to hedge at these significantly stronger levels.

Strategic implications for borrowers

The common theme across rates and FX is clear: expectations can reprice quickly, particularly when energy markets are in play. Moves in oil don’t just stay in commodities — they feed into inflation expectations, rate paths and currency dynamics, often faster than many anticipate. For borrowers, this isn’t just market noise. It’s a reminder that waiting for “certainty” can be costly. Hedging decisions should be anchored in longer-term risk tolerance and balance sheet resilience, rather than reacting to short-term swings that can reverse just as quickly as they appear.

Stay updated on market developments

Subscribe to receive our market insights and webinar invites

About the author

-

Jackie Bowie

Managing Partner

Head of EMEALondon

Jackie Bowie is a Managing Partner and Head of EMEA providing guidance and strategy for the European and APAC regions, with over 25 years of financial markets expertise.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

26-0022