BoE holds rates in a close vote; ECB stays on hold

Summary

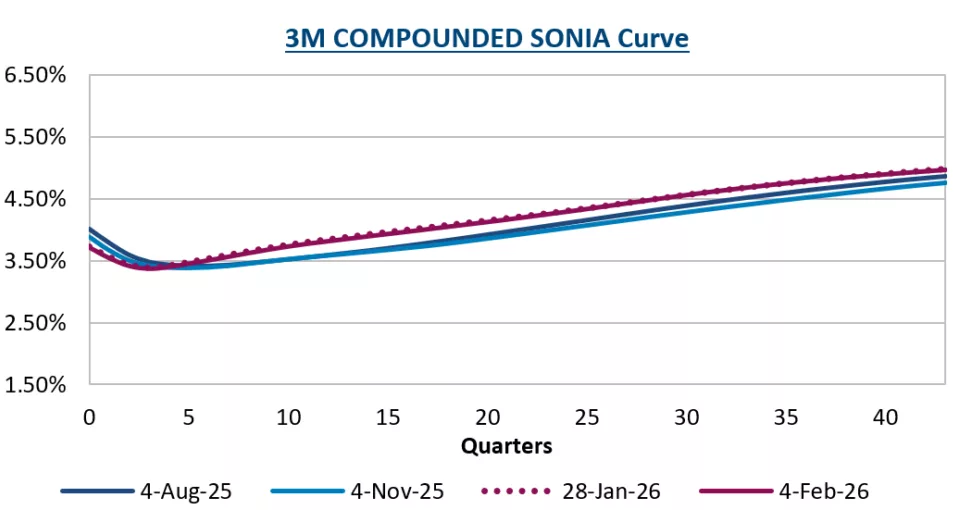

The Bank of England’s (BoE) Monetary Policy Committee (MPC) narrowly voted 5-4 to leave rates unchanged at 3.75%, with four members preferring a 25 basis point (bp) cut to 3.50%. Markets had expected a 7-2 vote, and the narrower margin quickly led investors to price in the higher probability of a cut in March.

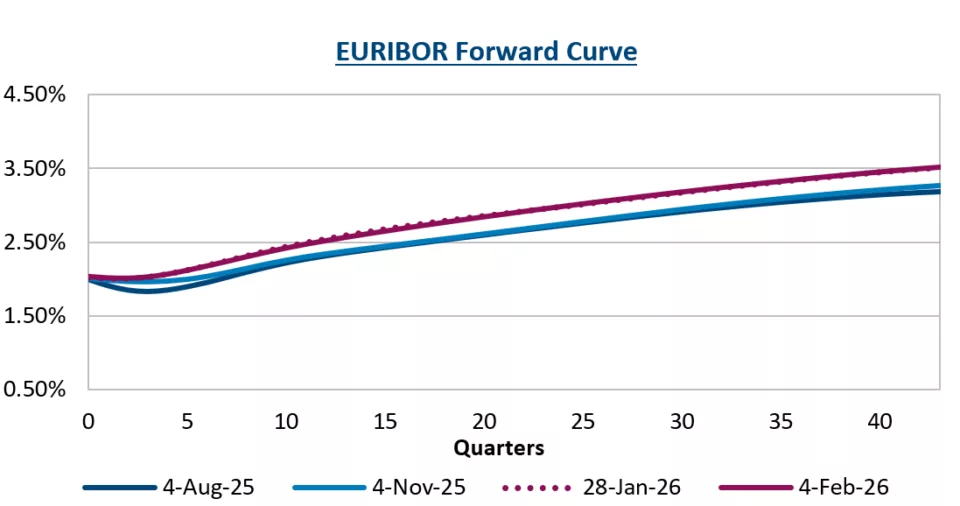

The European Central Bank's (ECB) Governing Council kept its three key rates unchanged, as expected, reiterating that policy decisions will remain data-dependent and taken on a meeting-by-meeting basis. The message stressed resilience amid uncertainty, with no pre-commitment to a future rate path.

Bank of England

While the BoE held Bank Rate at 3.75%, the committee’s 5–4 split suggests it is closer to lowering rates again. Four members voted for an immediate 25 bp cut, reflecting growing confidence that disinflation is becoming more durable. That contrasts with the December meeting, when policymakers emphasized caution around lowering borrowing costs further.

Markets reacted swiftly. The probability of a 25 bp cut in March rose to almost 50%, according to levels implied by swaps markets, from roughly 20% before Thursday’s decision.

The BoE expects CPI inflation to fall back toward target from April, helped by “developments in energy prices,” including measures introduced in last year’s Budget to curb increases in household bills. At the same time, the minutes emphasize subdued growth, increasing economic slack, and a labour market they forecast to continue loosening.

Further easing concerns, the Bank’s latest analysis of wage growth from its own survey shows expectations for this year have eased to a level consistent with the 2.0% inflation target. This reduces fears of a persistent feedback loop between high wages on the input side and high prices on the output side.

Governor Andrew Bailey struck an optimistic tone, saying, “My main message today is one of good news.” Disinflation is on track and inflation should return to around the 2.0% target “nearly a year earlier than we expected in November.”

Source: Chatham Financial

European Central Bank recap

The ECB kept rates unchanged, as expected, and repeated that it will remain data-dependent and avoid pre-committing to a rate path, stressing that its inflation outlook remains largely unchanged. The Governing Council tied future decisions to the inflation outlook and risks, underlying inflation dynamics, and the strength of monetary policy transmission, assessed using incoming data at each meeting. In its press conference, the ECB highlighted that inflation fell to 1.7% in January, from 2.0% in December, with core inflation also easing. It also pointed to encouraging GDP growth in Q4 2025, and unemployment that returned to a record low of 6.2% as evidence the economy remains resilient, even amid global trade and geopolitical uncertainty and a stronger euro. President Lagarde also addressed FX movements that recently saw the weakening trend of the U.S. dollar accelerate. Lagarde said, "What we observed collectively is that the dollar has depreciated measurably against the euro, but not in the last few days, but since March 2025. A stronger euro could bring inflation down beyond current expectations, more volatile and risk averse, financial markets could weigh on demand and thereby also lower inflation." Lagarde repeated that monetary policy is “in a good place” and while acknowledging that current policy settings are appropriate, Lagarde cautioned that “good” does not mean “static.”

Source: Chatham Financial

Moving forward

Following today’s narrow 5-4 split, market pricing implies a high probability of a BoE rate cut by the summer, with expectations for approximately two 25 basis points cuts over the remainder of 2026. The acceleration of inflation and slow path of disinflation, partly due to government policies on employment tax and pay, likely meant the BoE will continue to tread carefully in the months ahead.

Given exceptionally high domestic savings and a strong labour market, economists expect consumption to keep the eurozone economy growing, with the German government's planned fiscal splurge on defence and infrastructure a further push to expansion. This provides the council with confidence that downwards inflationary pressures won't persist over the medium term, and reinforced the case for keeping rates on hold for the foreseeable future.

Subscribe to receive our market insights and webinar invites

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

26-0012