FOMC holds rates, maintains mildly restrictive stance

Summary

On Wednesday, March 18, 2026, the Federal Open Market Committee (FOMC) voted to hold the federal funds rate unchanged at a range of 3.50%–3.75%. All members supported the decision except Governor Miran, who dissented in favor of a 25 basis point (bp) cut. The Committee emphasized increased uncertainty in the economic outlook, citing recent developments in the Middle East and their unclear implications for the U.S. economy. While economic activity continues to expand at a solid pace and unemployment remains stable, the housing sector remains a weak point.

The updated Summary of Economic Projections (SEP) showed upward revisions to both real GDP and PCE inflation relative to December. The expected rate path remained largely unchanged, however, with one cut projected in 2026 and another thereafter. Chair Powell reiterated that the Fed remains focused on its dual mandate and is monitoring risks on both sides. He highlighted ongoing concerns around inflation progress, particularly with goods prices. He also emphasized that policy would remain data dependent and that rates are currently near the boundary between restrictive and non-restrictive, with a preference to maintain mildly restrictive conditions until clearer inflation progress is achieved.

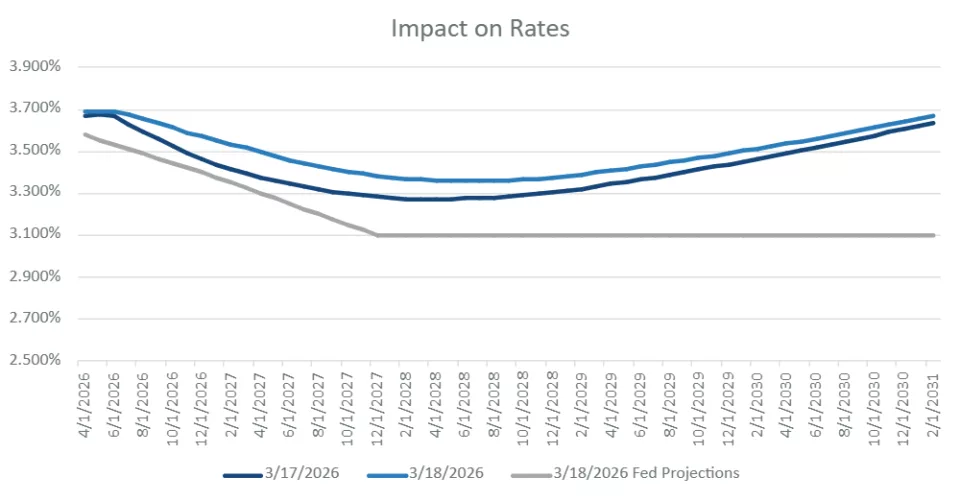

Impact on rates

Treasury yields moved modestly higher following Chair Powell’s press conference, reflecting a somewhat hawkish tone with a roughly 6 bps increase across the curve relative to pre-speech levels. While the Committee held rates steady, as expected, Powell’s emphasis on limited inflation progress and the need to maintain mildly restrictive policy reinforced a higher-for-longer narrative in the near term. His explicit statement that rate cuts are unlikely without further inflation improvement helped anchor front-end rate expectations.

The unchanged policy path in the SEP provided limited incremental dovish signals to offset the tone of the press conference. Powell noted that a hike is not the base case for most Committee members, which may help cap more significant upward pressure on yields, particularly at the front end. However, continued uncertainty surrounding geopolitical developments and the potential for oil-driven inflation contributed to a cautious market response.

The combination of stable labor market conditions, modestly higher growth and inflation projections, and the Fed’s continued focus on goods inflation suggests that the front end of the curve will remain sensitive to incoming inflation data. Meanwhile, longer-dated yields appear to be balancing improved growth expectations. This is driven in part by productivity and AI investment with lingering macro uncertainty. The result has been relatively contained but upward-biased rate movements following the meeting.

Source: Chatham Financial

Moving forward

Looking ahead, the Fed’s path remains firmly data dependent. Progress on inflation, particularly within goods, will be the primary driver of future policy decisions. Chair Powell made clear that without further improvement rate cuts are unlikely, reinforcing the importance of upcoming inflation data in shaping expectations.

At the same time, the Committee acknowledged that recent shocks, including higher oil prices tied to geopolitical developments, complicate the inflation outlook. The scope and duration of these effects remain uncertain.

Labor market conditions remain stable, with a low breakeven rate for new job creation and relatively steady unemployment since September. However, Powell noted emerging downside risk, suggesting the Fed is monitoring for signs of softening even as current conditions hold. The Committee also emphasized that SEP projections do not commit policymakers to a fixed rate path, underscoring continued flexibility to evolving data.

Broader factors add further complexity. Expectations for tariff-related inflation to ease around midyear, along with the potential for AI-driven investment to lift the neutral rate in the near term, shape the forward view. While markets are pricing a high likelihood of no change at the April meeting, the balance of risks across growth and inflation, and continued geopolitical uncertainty, will play a key role in determining the timing and magnitude of any eventual policy shifts.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

26-0028