BoE holds rates amid high inflation, ECB signals policy on hold

Summary

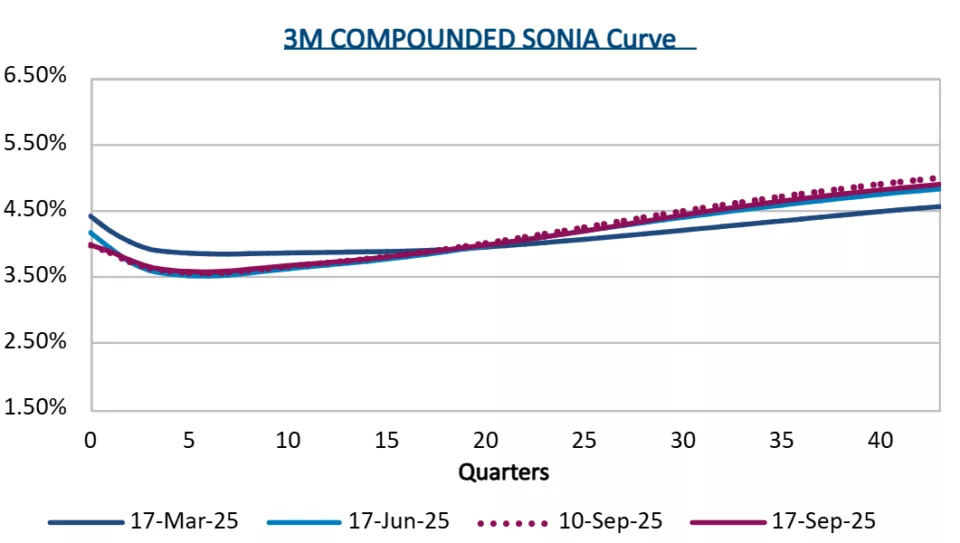

The Bank of England left the Bank Rate unchanged at 4.00% today as expected. Seven of the nine monetary policy committee (MPC) members voted to keep rates on hold, while two favoured another 25-basis-point cut. The MPC also announced a slowing in quantitative tightening to £70bn of gilt sales over the next 12 months. Policymakers warned of upside risks to inflation, which is currently above the Bank’s 2.0% target. Governor Andrew Bailey struck a cautious tone, saying inflation should ease, but “we’re not out of the woods,” so any future cuts will be gradual.

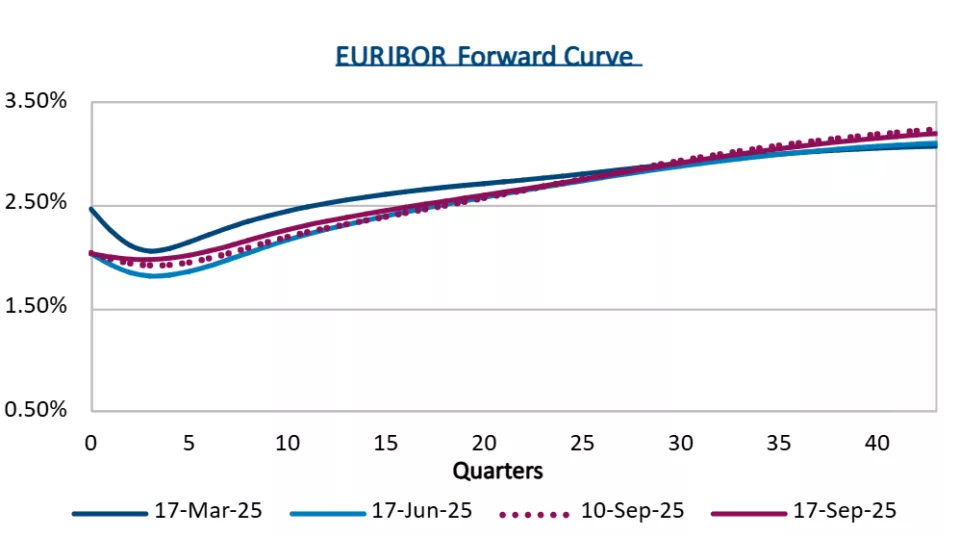

The European Central Bank held its key interest rates steady in September, as expected, with the deposit facility at 2.00% and the main refinancing rate at 2.15%. The decision was unanimous and the tone from President Christine Lagarde was relatively neutral, suggesting a steady, cautious, and data-dependent policy path. Having reduced rates eight times since mid-2024 and the ECB expressing greater optimism, or less pessimism, about the economic outlook, the recent pause suggests that policy will be on hold for the time being.

Bank of England recap

The BoE proceeded as expected, given that headline consumer price inflation is running at 3.80% and wage growth is still tracking just below 5.0%, despite mixed employment data. The two members of the MPC who voted to cut rates noted signs of “emerging slack” in the labour market and an expectation that the inflation hump would “normalise.”

The MPC repeated its guidance from August that “monetary policy was not on a pre-set path,” and that "a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate.” Governor Bailey emphasized that while inflation is expected to cool, policy must remain cautious.

The market reaction was muted, with little change in sterling and long-term UK sovereign borrowing costs relatively stable, having eased back from recent multi-decade highs this month. Market pricing suggests a low probability of a rate cut this year, with overnight index swaps implying approximately 8 basis points of easing priced in. The next 25-basis-point cut is not priced fully until spring 2026.

European Central Bank recap

For the European Central Bank, the decision to hold rates again was straightforward. Inflation is back at their target and while there are still pockets of weakness in the eurozone economy, the outlook is more positive than a few months ago. Concerns over a deterioration in economic growth due to the tariffs have eased and with them, risks that further disinflation could require policy to be set at a more accommodative level.

Staff projections show headline inflation for the euro-area averaging approximately 2.1% in 2025, falling to 1.7% in 2026, and rising slightly to 1.9% in 2027. The stronger euro, particularly versus the U.S. dollar, is a likely contributor to the forecasts for next year’s softer inflation rate.

Growth was revised up for 2025, now 1.2%, compared to June’s projections of 0.9%, and 2026 growth is seen at approximately 1.0%. ECB President Lagarde repeated her view that policy “continues to be in a good place.”

Market expectations for further rate cuts have diminished, and while some analysts think December could bring one more cut, market pricing suggests a low probability.

Moving forward

Looking ahead, the U.K. economy faces another fiscal hurdle in November, with the chancellor expected to raise taxes again to cover budget shortfalls from reversed spending cuts and higher borrowing costs. Depending on where these land, they could well cause the economy to slow and/or risk keeping inflation elevated, as businesses pass on increased tax through prices.

The BoE will likely focus on services inflation and pay growth, both of which need to cool further to build confidence that inflation will sustainably return to 2%.

In the eurozone, fiscal policy in major euro-area countries, especially under political stress (e.g. France), could also influence how the ECB shapes policy in the months ahead.

While it can feel like some relief that the trade situation has eased and should prove less of a drag on economic growth, the region still needs to be wary of further euro appreciation, potential U.S./China or U.S./EU trade frictions, and supply chain issues.

Subscribe to receive our market insights and webinar invites

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

25-0085