December rate cut not a foregone conclusion

Summary

On Wednesday, October 29, 2025, the Federal Open Market Committee (FOMC) voted to cut the Federal Funds rate by 25 basis points (bps), to a target range of 3.75%-4.00%. This marks the second cut in 2025, following ongoing concerns about the weakening U.S. labor market and rising unemployment. In the midst of a government shutdown that is now approaching the 1-month mark, the FOMC cited “available indicators” in light of the delays in federal economic data releases. The Committee reaffirmed its dual mandate of promoting maximum employment and returning inflation to 2%. The statement released reiterated that job gains slowed this year, the unemployment rate edged up, all while inflation has slightly increased since earlier in the year and remains somewhat elevated. Newly appointed Fed Governor Stephen Miran dissented against the Committee’s decision for the second straight meeting, in favor of lowering rates by 50 basis points. Kansas City Fed President Jeff Schmid also dissented, but against a rate cut altogether. This is the first time we have seen dissents on each side of a decision since 2019. The Fed also announced that its balance sheet runoff will end on December 1, 2025. The Fed board will continue to monitor data to guide its decisions.

Impact on rates

In what appeared to be a direct response to Chair Powell’s statement that another 25 bp cut in December is “not a foregone conclusion,” swap rates increased by 2-3 bps across the curve. The market is now pricing a 40% chance of no rate cut in December, up from 9% yesterday and 4% a week ago. The forward curve now projects three more 25 bp cuts by the end of next year, with the target range ending 2026 between 3.00%-3.25%. 2-year Treasury yields were up 9 bps with the 10-year up 5 bps. Chair Powell’s comments at the press conference, specifically related to the next meeting in December, signaled that the Committee is not on a pre-set course. Powell continues to affirm that the Committee will remain data dependent despite the limited available government economic data due to the government shutdown.

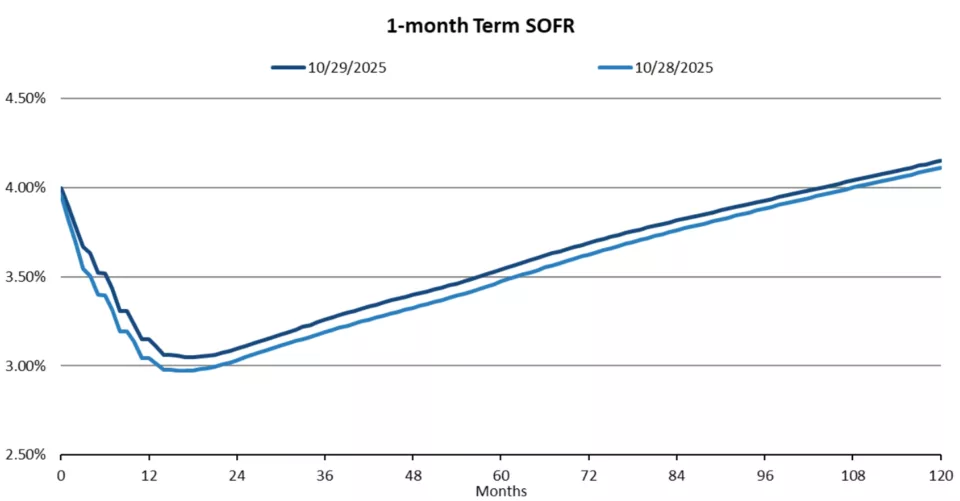

Source: Chatham Financial

Moving forward

In line with Powell’s rhetoric, expect the market to remain focused on inflation and the U.S. labor market, despite delays in some data releases due to the government shutdown. If the labor market continues to show signs of weakening (supporting the need to cut rates) or inflation persists above the target range (supporting fewer rate cuts) there is potential for further dissent among the Committee members on both sides of the policy spectrum. Powell stated that economic activity has been rising at a moderate pace, but the higher downside risk has shifted to the labor market. Starting December 1, the Fed will end Quantitative Tightening (QT) and hold its balance sheet steady following the gradual reduction of $2.2 trillion over the past three years. As non-Treasury bills mature, the Fed will purchase treasury securities as replacements to maintain its balance sheet. The Fed’s statement noted that economic uncertainty remains elevated, and the Committee will continue to be attentive to both sides of its dual mandate.

Subscribe to receive our market insights and webinar invites

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

25-0105