BoE and ECB keep rates on hold but both warn of inflation risks amid Middle East conflict

Summary

The Bank of England’s (BoE) Monetary Policy Committee (MPC) voted unanimously to keep interest rates at 3.75% today, as they warned of a rising risk to the path of inflation and economic outlook from the worsening conflict in the Middle East. While the decision itself was widely expected, the tone was materially more hawkish than markets had been pricing previously, with all four MPC members who voted in favour of a 25 basis point (bp) cut last month, voting to now keep them on hold.

The European Central Bank (ECB) also left its three key policy rates unchanged and warned that the war in the Middle East has made the outlook “significantly more uncertain,” creating upside risks to inflation and downside risks to growth. The ECB’s updated staff projections now see headline inflation averaging 2.6% in 2026, up from 2.0% in their December forecasts, with the revision driven largely by higher energy prices.

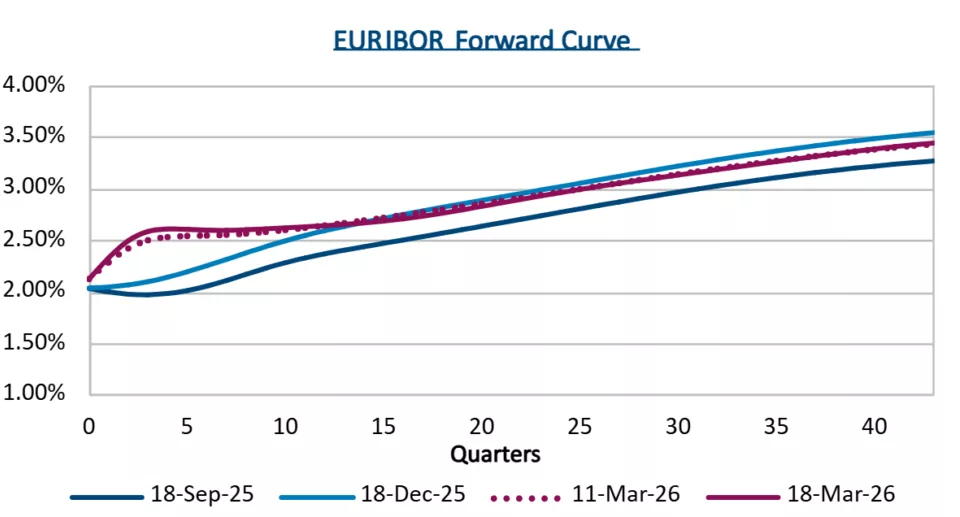

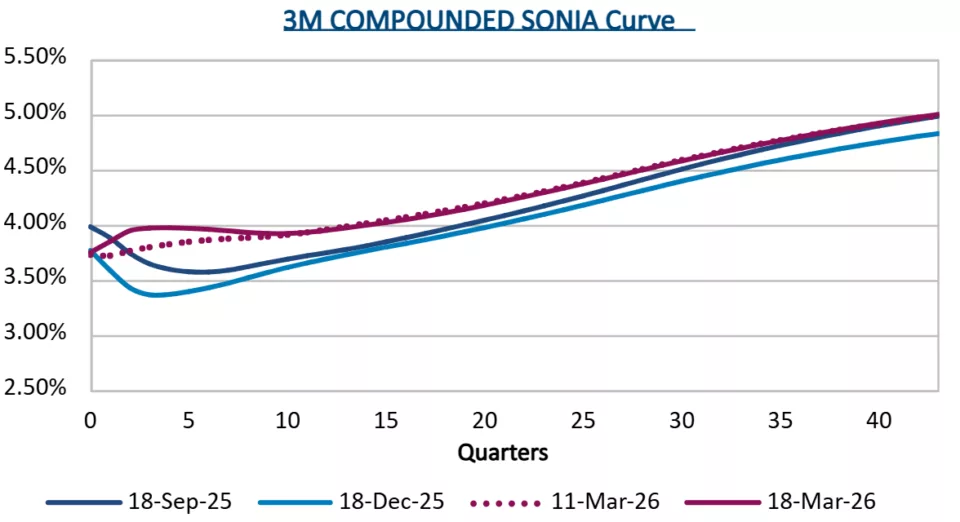

Rates markets have responded accordingly. Sterling swap rates have risen materially, with the 5-year GBP swap rate near 4.25% today versus 3.60% prior to the commencement of US-Israeli strikes, while the 5-year EUR swap rate has risen to 2.70%, from 2.30% over the same period.

In FX markets, the GBP saw another volatile day, reversing an earlier decline versus the U.S. dollar to 1.3250, reaching an approximate 1.0% gain to 1.3400. The Euro also finished the day around 1.0% higher versus the dollar at 1.1550.

Bank of England

The BoE kept borrowing costs on hold, but the message was notably firmer than in February. In the minutes, the MPC said it is alert to the risk that higher energy prices could feed into domestic inflation through second-round wage and price-setting effects. It also stressed that a more prolonged shock could require a more restrictive policy stance.

The Bank’s updated near-term inflation profile shifted meaningfully higher. Based on current energy prices, which have effectively doubled since the conflict began, the MPC said CPI inflation is now expected to rise to around 3.0% in Q2, rather than the 2.1% it had forecast in the February Report. In Q3, it could rise to 3.5%,, with energy prices contributing around 0.75%.

At the same time, this morning’s UK labour market data pointed to a soft domestic backdrop that would ordinarily support monetary policy easing. While the unemployment rate was unchanged at 5.2% in the three months to January, payroll data showed a decline over the same period and regular pay growth slowed to 3.8%, the weakest pace in roughly five years.

Before the latest energy shock, the BoE itself noted subdued economic growth, weak labour demand, and slowing private sector pay growth would allow the Bank to continue easing monetary policy. MPC member Dave Ramsden remarked that he would otherwise have voted for a 25 bp cut.

However, in televisions interviews following the Bank’s announcement, BoE governor Andrew Bailey stressed that the “appropriate thing” was to hold interest rates at this point, saying “I would caution against reaching any strong conclusions about us raising interest rates.”

Source: Chatham Financial

European Central Bank

The ECB also kept rates unchanged, leaving the deposit facility at 2.00% and the main refinancing rate at 2.15%. The Governing Council said it remains committed to returning inflation sustainably to 2.0% but emphasized that the Middle East conflict has materially increased uncertainty, and energy prices would have a material impact on inflation in the short term.

The updated ECB projections show headline inflation averaging 2.6% in 2026 but will return to their 2.0% target in 2027. However, they warn that the energy shock would hit growth markedly this year, with growth seen at 0.9% in 2026, compared with 1.2% previously forecast. The ECB said the revised inflation path and growth outlook were primarily because of higher energy prices. However, there were no immediate signs of panic among the governing council, with ECB president Chistine Lagarde commenting that medium-term inflation expectations remain anchored.

President Lagarde also said the medium-term implication of the surge in energy prices “will depend both on the intensity and duration of the conflict and on how energy prices affect consumer prices and the economy.”

From a markets perspective, the ECB’s apparent calm approach helped 5-year euro swap rates ease back slightly from their highs of 4.30% immediately after today’s BoE and ECB rate announcements but remain well above late-February levels.

Source: Chatham Financial

Moving forward

For sterling markets, the near-term tension is now clearer. Softer U.K. labour market data and moderating wage growth would typically support a continuation of easing to support economic activity, but the BoE’s reaction function has shifted because of the unexpected major energy shock.

The BoE’s deputy governor said she was previously expecting to vote for a quarter-point rate cut, but the Iran conflict had forced her to reconsider, saying, “Monetary policy cannot influence global energy and commodity prices, but it can and it must aim to ensure that the economic adjustment to them occurs in a way that achieves the 2 per cent target sustainably.”

The ECB appears more confident that inflation expectations in the euro area remain anchored and that the economy retains a degree of resilience. However, it is now navigating a more challenging backdrop of higher near-term inflation and weaker growth. While the experience of Russia curtailing energy supplies following its 2022 invasion of Ukraine may leave the bloc better prepared for energy shocks than before, both household and business sentiment are unlikely to escape the impact. This comes at an unwelcome moment, just as the economy had been showing encouraging signs of recovery.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

26-0029