Hairy charts: the accuracy of SOFR, SONIA, and EURIBOR vs. historical LIBOR forward curves

Summary

The forward curve serves as a baseline projection of future interest rates to support investment analysis. Borrowers can use it to evaluate potential costs and returns on investments. While not a precise forecast, forward curves can help borrowers identify potentially advantageous times to transact, such as locking in rates or extending hedges.

Key takeaways

- Borrowers use forward curves to assess hedging strategies for current and future financing, helping to mitigate risks associated with interest rate volatility.

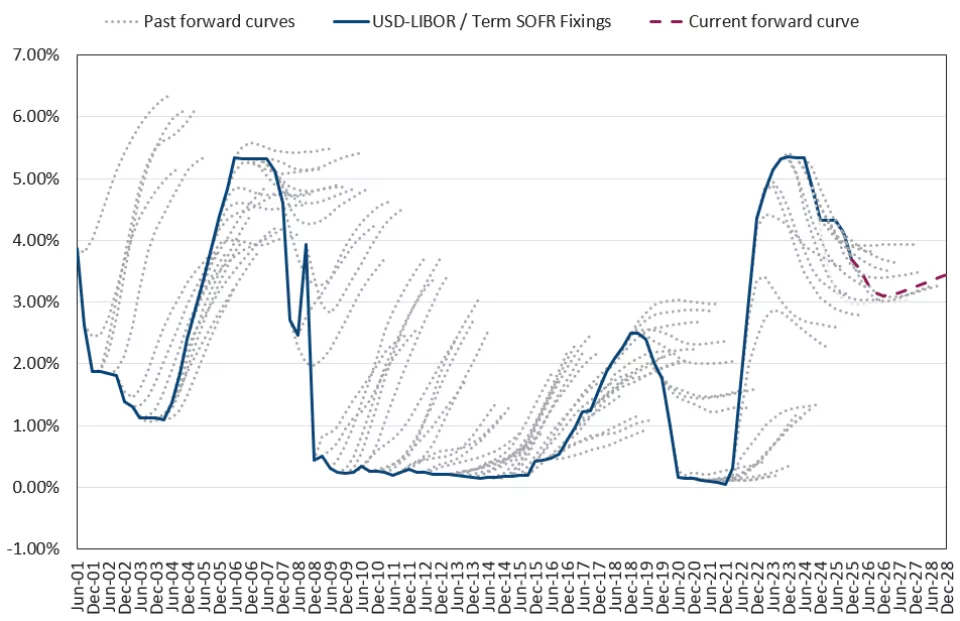

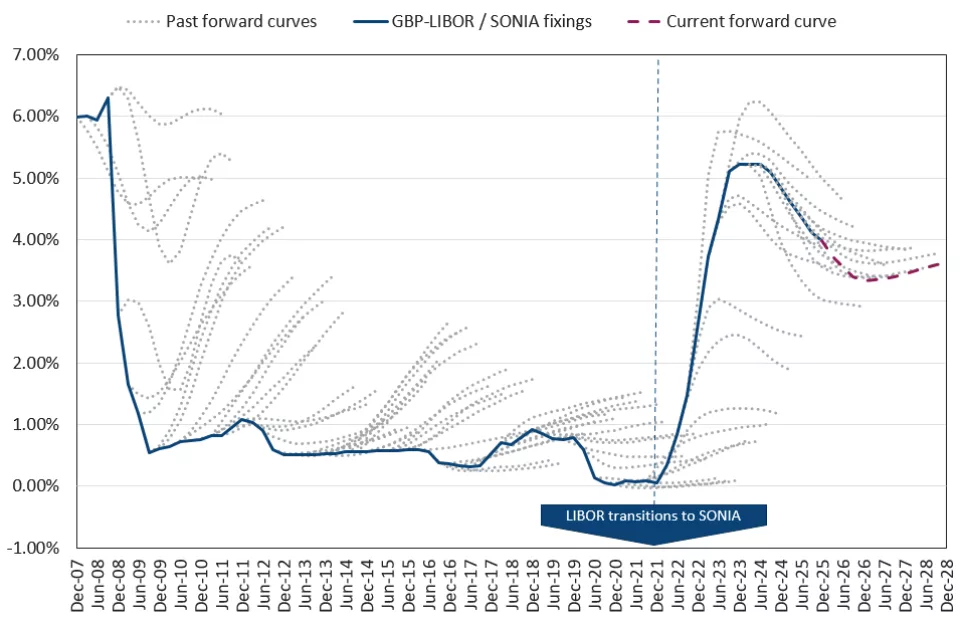

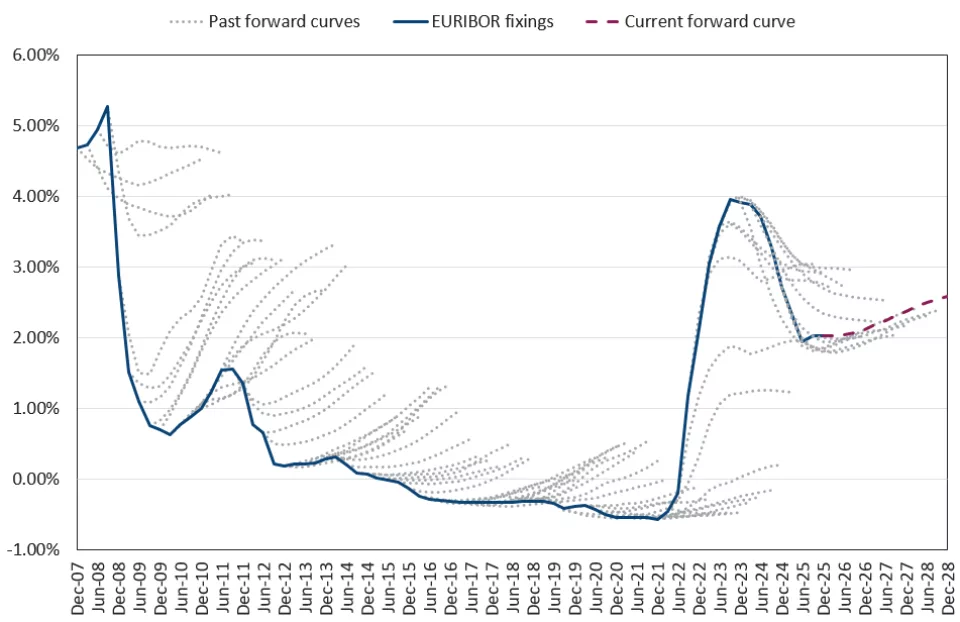

- All LIBOR settings permanently ceased in September 2024: USD LIBOR forward curve transitioned to Term SOFR in 2023; GBP LIBOR transitioned to SONIA in 2021; and EURIBOR remains.

- The hairy chart illustrates how market expectations (represented by the forward curves) compare to actual rate movements, giving you insight into market sentiment and potential biases.

The graphs below plot the past forward curves over the actual path LIBOR followed and its new benchmark after the transition. They show that the forward curve has been a somewhat accurate predictor over the next six months or so, pricing in more foreseeable market events in the near term. Beyond that, they have not generally been accurate as the market does not predict further and less certain events. This is the reason for the significant delta or “error” in forward rate predictions, particularly exaggerating the error when significant unanticipated events move LIBOR.

The forward curve remains an important base case for underwriting, with most investors adding a variety of scenarios for stress testing.

1-month USD LIBOR / Term SOFR vs. historical forward curves

Revised December 31, 2025

3-month GBP LIBOR / SONIA vs. historical forward curves

Revised December 31, 2025

3-month EURIBOR vs. historical forward curves

Revised December 31, 2025

What is the hairy chart?

Dive deeper into how forward curve projections are rarely right, but still valuable inputs for underwriting.

Ready to have weekly rates and capital markets insights delivered to your inbox?

Subscribe for industry insights