BoE narrowly votes to cut interest rates, ECB signals their cutting cycle may be complete

Summary

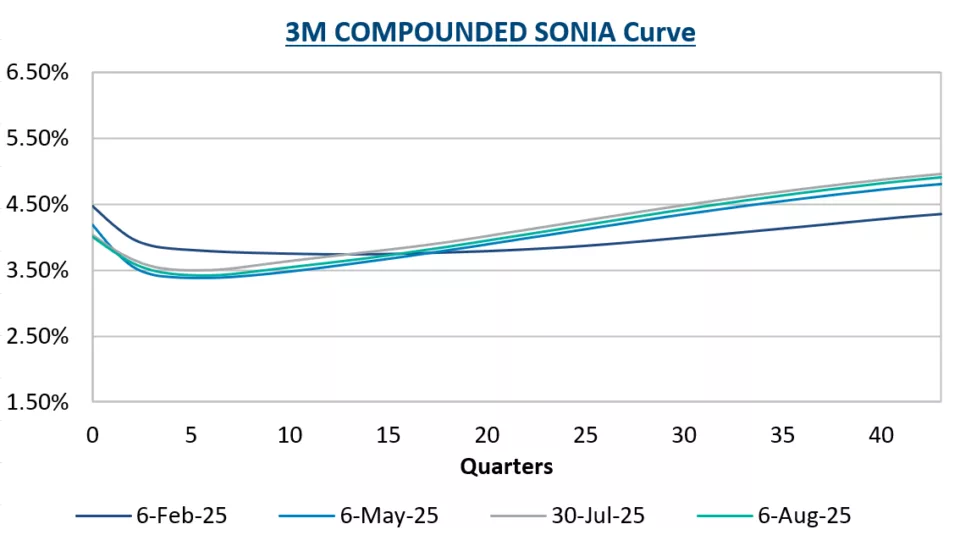

Today, the Bank of England cut its Bank Rate by 25 basis points to 4.0%, the fifth reduction over the last year and the lowest level since March 2023. The decision was highly contested, requiring two rounds of voting for the first time in the bank’s history, with a 5‑4 split. One member broke the tie after initially voting for a larger cut. The tone of the press conference was cautious and balanced, with Governor Andrew Bailey stressing the need to proceed “gradually and carefully” against a backdrop of conflicting signals.

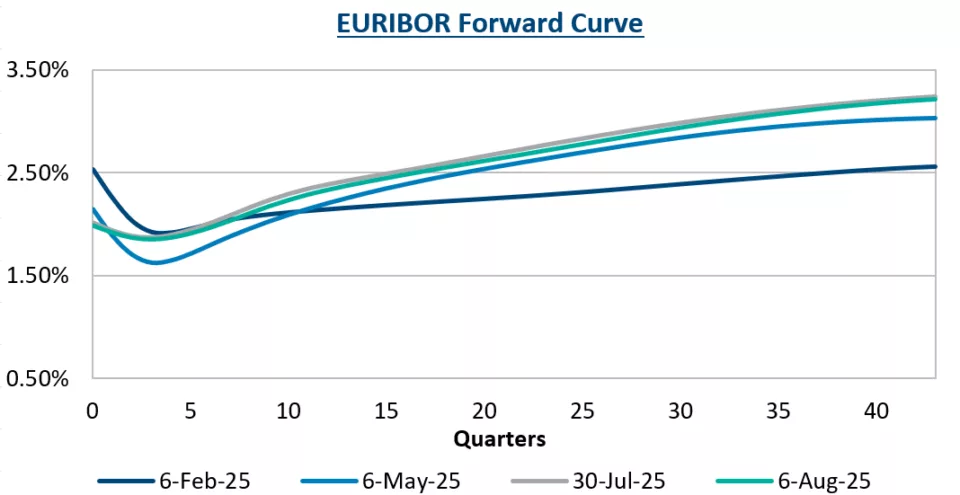

The European Central Bank opted to hold interest rates steady at its meeting last month, pausing after a series of eight cuts totaling 200 basis points since June last year. The decision was unanimous, reflecting growing confidence that inflation has stabilized around the 2.0% target. The ECB’s tone was also cautious, marked by concern over global trade uncertainties. Although, this was prior to the EU-U.S. trade deal framework announcement that reduces the tariffs to 15% from 30%.

Bank of England

Today’s rate cut decision was much closer than the market was expecting, with the bank’s Monetary Policy Committee (MPC) splitting over whether to lower rates or keep them on hold. One MPC member had initially pushed for a 50 bp, before aligning with the narrow majority in favour of the more modest 25 bp reduction.

Governor Andrew Bailey said, “We’ve cut interest rates today, but it was a finely balanced decision,” while suggesting that the path of interest rates “continues to be downward”. However, he added that there was now “genuine uncertainty” because the MPC saw risks of both inflation overshooting its forecasts and growth undershooting.

Bailey cautioned against moving too quickly with further cuts, noting that hasty easing could entrench inflationary expectations.

The bank will certainly have to tread carefully, with consumer price inflation having risen to 3.6% in June and at the BoE’s forecast of a peak at 4.0% this year, amid upward pressure from the minimum wage increase, payroll tax increase, as well as surging food prices.

All of which makes for a rather difficult period for the economy, which is facing challenges from the macroeconomic perspective, as well as further talk of tax hikes due to the government’s failure to cut spending.

The immediate market reaction was a broad strengthening of the pound, which gained one cent against the U.S. dollar and the euro, as well as a rise in U.K. government bond yields.

European Central Bank

Following eight consecutive 25 bp rate cuts, lowering the deposit facility rate to 2.0% and similarly reducing the main refinancing and marginal lending rates, the ECB kept rates on hold. The Governing Council emphasized that inflation has been hovering close to its 2.0% target, wage growth is moderating, and the eurozone economy has shown relative resilience despite external pressures.

However, the statement reflected that the macro environment remained challenging, noting, “The environment remains exceptionally uncertain, especially because of trade disputes,” adding that its inflation and growth outlook from June remained supported by recent data.

At the press conference, ECB President Christine Lagarde said they expected a quick resolution in trade tensions along with higher European defense and infrastructure spending, which could boost growth in the coming months more than previously forecast. With a trade framework agreed upon, but tariffs on most EU goods still at a relatively high 15%, the risks still look tilted to the downside.

Nevertheless, with the bar for further rate cuts seemingly set quite high, the euro strengthened across the board and bond yields rose modestly.

Moving forward

While the BoE is still expected to lower rates, market pricing suggests much less conviction following today’s meeting. The chance of another 25 bp cut before the end of the year stands at around 70%, though as the bank stated, this remains entirely data-driven and will depend on upcoming inflation and labour market data.

Markets are currently pricing an approximate 80% chance of another 25 bp cut from the ECB by the first quarter next year. The ECB’s shift to a data‑driven, meeting‑by‑meeting approach suggests it will closely monitor developments in inflation, wages, credit, and global trade tensions before making further moves.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

Transactions in over-the-counter derivatives (or “swaps”) have significant risks, including, but not limited to, substantial risk of loss. You should consult your own business, legal, tax and accounting advisers with respect to proposed swap transaction and you should refrain from entering into any swap transaction unless you have fully understood the terms and risks of the transaction, including the extent of your potential risk of loss. This material has been prepared by a sales or trading employee or agent of Chatham Hedging Advisors and could be deemed a solicitation for entering into a derivatives transaction. This material is not a research report prepared by Chatham Hedging Advisors. If you are not an experienced user of the derivatives markets, capable of making independent trading decisions, then you should not rely solely on this communication in making trading decisions. All rights reserved.

25-0072