Recapping Powell's Jackson Hole 2022 speech

Summary

Chair Powell’s speech today at Jackson Hole was all about inflation, a notable shift from the 2021 Jackson Hole symposium which was more focused on the labor market. The speech concentrated on three key lessons the central bank has learned: taking key responsibility for delivering low and stable inflation, the importance of the public’s inflation expectations on the actual path of inflation over time, and keeping at it until the job is done.

Key takeaways

- Powell insisted that the Federal Reserve must “keep at it until the job is done”, and sees greater risks skewed toward stopping rate hikes prematurely vs. maintaining a more restrictive policy.

- Powell warned that “reducing inflation is likely to require a sustained period of below-trend growth” with “some softening of labor market conditions”.

- Powell reinforced that current inflation in the U.S. is a product of a supply-demand imbalance, acknowledging that the Fed’s primary tools to restore this balance work is by tightening financial conditions and reducing aggregate demand in the economy.

- Short-term rates spiked immediately on this hawkish messaging but have come in over the course of the day.

- Market are pricing a 40%/60% probabilities of a 50 bps/75 bps hike from the Fed at their September 21 meeting.

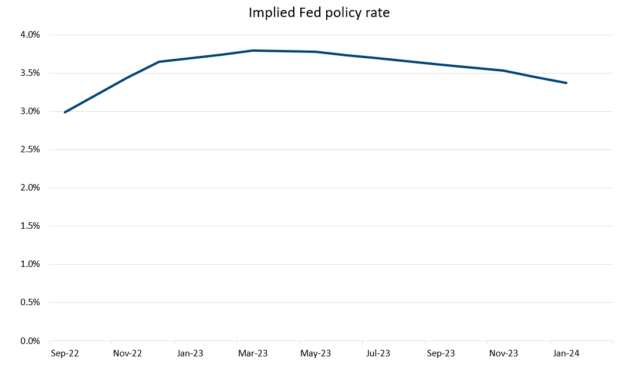

The Fed sent a key message to the markets today: they take their mandate to taper inflation seriously and are willing to maintain restrictive monetary policy until inflation comes down, even if that means inflicting some pain on the economy. The Fed most recently raised their benchmark rate by 75 basis points to 2.25%–2.50% in their July meeting and the market currently expects a toss-up between a 50 bps and 75 bps hike during the September 20–21 meeting. Current forward curves are pricing the fed funds rate to top out in the 3.75%–4.00% range by March 2023 and ultimately settling around 3.50% by the end of 2023. Over the next few weeks, key economic data that will influence the Fed include the jobs report on September 2 and the consumer-price index report on September 13.

Pricing as of August 26, 2022

One key quote from the speech references former Fed Chair Paul Volcker’s fight against inflation in the 1980s. Powell notes that, “a lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year”. The messaging here is intentional and makes a clear point that battling inflation is the first priority and some labor market softening will be tolerated. While inflation pulled back slightly in July with pricing falling 0.1% vs. June, this was specifically noted as something that “falls far short of what the Committee will need to see before we are confident that inflation is moving down”.

The Fed’s tools primarily work by influencing the demand side of the economy – raising rates increases the cost of capital, which increases return hurdles and reduces risk-taking appetite, ultimately slowing economic growth. At the start of the COVID-19 pandemic, the United States saw a supply shock as the world shut down coupled with a demand shock from both accommodative monetary policy and fiscal stimulus. Monetary policy has recently shifted toward a restrictive/tightening Fed while the fiscal side has seen continued stimulus from the American Rescue Plan in 2021, and more recently the CHIPS Act, Inflation Reduction Act, and proposed student loan forgiveness.

Plenty of questions remain on the supply side. Some supply-chain bottlenecks are easing as retailers have stocked up inventories and consumers have shifted spending toward services due to pent-up travel demand. However, geopolitical tensions raise a new host of potential issues. The Russia-Ukraine war has generated major shocks to global food and energy supplies. The impacts are most acute in Europe where power costs are skyrocketing. For example, German and French natural gas prices are up over 10-times from earlier this year. The immediate impact is an upward shock to prices, but the medium- and long-term implications are less clear if these shocks result in factory shutdowns.

Longer-term questions also remain – have we passed peak globalization and turned to a period of re-onshoring manufacturing? More domestic manufacturing is likely to be inflationary via higher labor costs, increased domestic investment boosting commodity demand (and prices). If the recent historical period of low inflation is gone, what are the implications for the terminal rate? Is the forward curve correct that we’ll get to 3.75%–4.00% and ultimately settle around 3.50% or would a new high-inflation regime result in a higher neutral rate?

The current forward curve still projects that rates will moderate toward the second half of 2023 and inflation expectations remain anchored with 10-year Treasury inflation protected securities pricing in a 2.58% long-term annual inflation rate. All eyes will be on the upcoming CPI and jobs data over the next few weeks as the market tries to figure out the path going forward.

Subscribe to receive analysis and insights regarding the Federal Reserve policy updates

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

Transactions in over-the-counter derivatives (or “swaps”) have significant risks, including, but not limited to, substantial risk of loss. You should consult your own business, legal, tax and accounting advisers with respect to proposed swap transaction and you should refrain from entering into any swap transaction unless you have fully understood the terms and risks of the transaction, including the extent of your potential risk of loss. This material has been prepared by a sales or trading employee or agent of Chatham Hedging Advisors and could be deemed a solicitation for entering into a derivatives transaction. This material is not a research report prepared by Chatham Hedging Advisors. If you are not an experienced user of the derivatives markets, capable of making independent trading decisions, then you should not rely solely on this communication in making trading decisions. All rights reserved.

22-0218