Do interest rate swaps with floors make sense?

Have you wondered how an interest rate swap with an embedded floor works? What about the implications for using this structure?

When you add a floor to a loan, you are requiring your borrower to SELL the bank an option. The bank, however, doesn’t compensate the borrower for the cost of the option.

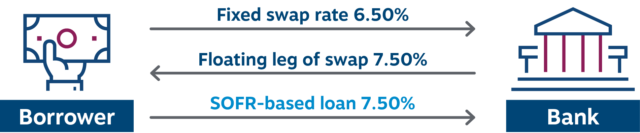

Let’s say we pair a normal interest rate swap with a loan that has a floor:

- The borrower could lock in a 10-year swap rate of 6.50% if the loan is priced at 1 mo. Term SOFR + 225 bps credit spread.

- The floor in the loan is at 3.00% on 1 mo. Term SOFR.

If 1 mo. Term SOFR stays at or above that strike, then the loan and swap work together in harmony and the borrower has a fixed rate of 6.50%.

Now let’s say 1 mo. Term SOFR is 2.75%, or 25 bps below the floor added in the loan. What happens?

- The borrower PAYS 6.50% on the swap and RECEIVES 5.00%, so the net swap payment is 150 bps.

- On the loan, the borrower pays not 5.00%, but 5.25% because there is a floor.

That means the borrower is paying 5.25% + 150 bps = 6.75%, or 25 bps MORE than the fixed swap rate.

What can be done with the example above?

- Do nothing, keep the floor in the loan and no floor in the swap. This will mean if 1 mo. Term SOFR goes below the floor strike, then the borrower’s cost of funds will increase (this is called an inverse floater).

- You can insert a floor in the swap. This has a downside, though. In the example shown, the borrower sold the bank the floor in the loan and did not get paid for it. Now the bank makes the borrower buy back that same floor in the swap, but the borrower must pay for it — at a higher swap rate. This example of a 10-year swap with a floor at 3.00% would add 65 bps to the fixed rate, taking it from 6.50% to 7.15%. This makes the bank’s offering uncompetitive, and the deal will likely be lost.

- Don’t put a floor in the loan IF THE LOAN WILL THEN BE SWAPPED; let ALCO or Treasury manage the bank’s interest rate risk and the yield of the loan book through macro strategies. This will be the path of least resistance.

Sometimes banks will add a 0% floor in floating rate loans, but not mirror the floor in the swap. If the borrower understands that if 1 mo. Term SOFR goes below zero, their “fixed” rate increases, then this is an acceptable solution.

Talk to Chatham about swaps

Speak with a Chatham representative to learn more about interest rate swaps or how to optimize your existing hedging program.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

Transactions in over-the-counter derivatives (or “swaps”) have significant risks, including, but not limited to, substantial risk of loss. You should consult your own business, legal, tax and accounting advisers with respect to proposed swap transaction and you should refrain from entering into any swap transaction unless you have fully understood the terms and risks of the transaction, including the extent of your potential risk of loss. This material has been prepared by a sales or trading employee or agent of Chatham Hedging Advisors and could be deemed a solicitation for entering into a derivatives transaction. This material is not a research report prepared by Chatham Hedging Advisors. If you are not an experienced user of the derivatives markets, capable of making independent trading decisions, then you should not rely solely on this communication in making trading decisions. All rights reserved.

23-0214