Defeasance pitfalls: What borrowers need to know

Summary

The intent of this piece is to bring awareness to some defeasance pitfalls, and return leverage to the hands of borrowers.For real estate borrowers seeking fixed-rate financing, CMBS debt can be an attractive option. The 10-year, fixed-rate loans offer LTV flexibility and competitive pricing on a non-recourse basis – features that can strengthen a pro-forma and complement a long-term strategy. But while CMBS can be accretive to returns, it can also impair them; borrowers that refinance or sell mid-term will be forced to repay loans early, triggering a potentially painful exit.

The culprit is defeasance – a form of call protection that typically carries a large premium and high fees. Unfortunately for borrowers, defeasance is here to stay. The protection that it provides bondholders is necessary to preserve demand, and is one of the reasons that CMBS can enjoy the term and pricing advantages highlighted above. While defeasance is necessary, conflicts of interest and hidden costs cause borrowers to pay more to defease than is necessary.

Process and parties

Importantly, a defeasance is not a prepayment of the mortgage loan. It is a collateral substitution of a high-quality bond portfolio in exchange for a release of the mortgage lien. Concurrent with the collateral substitution, the loan obligation and replacement securities are transferred to a third party (the successor borrower). The real estate is released to be refinanced or sold, and the successor borrower satisfies the remaining loan payments using income generated by the securities.

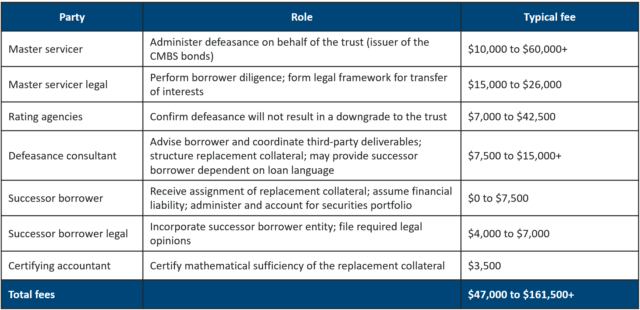

Transactions typically take 30 days to complete, require a new legal framework for the transfer of interests at closing, and rely on the cooperation of various third parties, each taking a fee:

Fees to third parties can add up, but will still represent just a fraction of the total costs to defease the loan. The most significant cost almost always results from the purchase of replacement collateral, which is explored in the following section.

Replacement collateral

The primary cost in defeasance is the purchase of the replacement collateral: a laddered portfolio of high-grade securities structured to meet all remaining debt service payments on the loan. Cost drivers include the number of years remaining on the loan, the type of securities permitted to be used, the prevailing interest rate environment, and the method of purchase. The loan documents will specify qualifying securities, but replacement collateral is often restricted to Treasuries only. In such a scenario, the cost of collateral roughly equals the sum of the present values of each remaining payment due on the loan, discounted by the yields of the respective Treasuries.

In a low interest rate environment, defeasance can be punitive. However, there are three key ways that borrowers can defray some of the cost:

- Higher yielding securities: Certain loans permit the use of “agency” securities, in addition to U.S. Treasury securities. These include bonds issued by Freddie Mac, Fannie Mae, the Federal Home Loan Banks, and other government agencies and typically price at a discount to Treasuries. The inclusion of these securities can materially reduce the cost of the portfolio. Whether or not agencies qualify as replacement collateral is determined at origination and written into the loan documents.

- Purchase via auction: At closing of the defeasance, a single bank delivers the securities to serve as replacement collateral. The bank’s interest is to maximize profit, so the only way to ensure lowest-cost execution is through a competitive bidding process, forcing banks to compete on margin. Auctions are increasingly vital when agency securities are permitted, as the agencies market is shallower than the Treasuries market and dealer inventories can vary substantially.

- Residual value: The successor borrower has the ability to recoup value from the replacement collateral in two ways: (i) reinvestment of any idle cash (cash received but not yet needed to make a loan payment), and (ii) early loan prepayment (taking advantage of a loan’s open prepayment window). This residual value can range from a few hundred dollars to hundreds of thousands of dollars, and can alleviate costs to the borrower.

Borrower cheat sheet

With limited control, high fees, and hidden costs, how do borrowers preserve value?

In the fight for a low-cost defeasance, most of the damage is done at loan origination. Unfavorable loan terms severely handcuff a borrower down the line, so it is important to know what to look for and why it matters.

Borrowers should be aware that the following provisions are negotiable in all fixed-rate CMBS loans (ideally at the term sheet phase, before a lender is awarded a deal):

Borrower should retain the right to designate the successor borrower. Originators may attempt to retain and sell this right to a third party. Borrowers that cede control over the successor borrower forgo two crucial abilities:

- The ability to recoup residual value. As described above, this value can easily reach six figures, and should accrue to the party paying for the defeasance (most often the borrower in a refinance, but occasionally the purchaser under a sale).

- The ability to extinguish the debt. Because the loan remains outstanding after defeasance, the risk of a default still exists. If a security fails to pay or the portfolio is structured incorrectly, then the Borrower and successor borrower may be held jointly liable. This can trigger serious accounting implications, as borrowers with contingent liability may need to continue to recognize the debt post-defeasance (an “in-substance” defeasance). If, however, the borrower controls the successor borrower, then the borrower can arrange for the successor borrower to assume default liability in isolation, and the borrower can consider the debt cancelled (“legal” defeasance).

Borrower should retain the right to purchase and deliver the replacement collateral. Originators may attempt to retain and sell this right to a third party, with potentially dire consequences for the borrower. This third party will charge an arbitrary fee to the borrower, and has no obligation or economic incentive to purchase an efficient, low-cost portfolio via auction. Often this same party will hold the successor borrower rights, creating misaligned incentives between the borrower and third party (an inefficient, higher cost collateral structure can directly increase the residual value accruing to the benefit of the third party and originator). This represents a direct conflict of interest and complete destruction of value to the borrower.

Flexible replacement collateral. Permitted replacement collateral should include the use of a wide variety of agency securities, and the loan should allow the collateral to provide for remaining payments, at borrower’s election, from the open prepayment date to any payment date thereafter through maturity.

Leverage the right defeasance consultant

Regardless of loan provisions, the defeasance consultant working on behalf of borrower can have a material impact on the timing, execution, and costs. The defeasance consultant acts as the borrower’s eyes and ears throughout the process, so borrowers should take special care to evaluate their partner prior to signing an engagement letter.

As hindsight is 20/20, borrowers should be wary of any consultant that does not volunteer the following:

- Sharing of residual value

- Assumption of default liability post-defeasance

- Assurance of purchase via auction

- Disclosure of past lawsuits

- Full disclosure of fees

Defeasance can be a frustrating and costly process, but it doesn’t have to be. Through education, awareness, and the aid of a good consultant, borrowers can eliminate conflicts of interest and sidestep hidden cost traps with maximum value intact.

Chatham Financial has executed over $177 billion total principal defeased, and returned over $200 million in residual value to borrowers. Defeasance consultants are a part of Chatham's global real estate financial risk management practice, solving common but complex capital markets challenges for commercial and multifamily real estate investors.

Need help with defeasance?

Contact a Chatham advisor about defeasance or yield maintenance.