Common hedge accounting terms

Summary

A guide to help understand frequently referenced topics and definitions of commonly used terms in hedge accounting.

Inception documentation

Formalizes the company’s election to achieve preferred hedge accounting on an executed derivative. This documentation must be completed contemporaneous to the election. It should contain four key components: identification of the hedging instrument, the hedged transaction, the nature of the risk being hedged, and how the hedging instrument’s effectiveness in hedging the exposure to the hedged transaction’s variability in cash flows attributable to the hedged risk will be assessed. This includes whether the assessment at inception will be on a quantitative or qualitative basis and how subsequent assessments will be performed.

Effectiveness testing

An effectiveness test is performed both at inception and ongoing period while the derivative is designated for hedge accounting. The method used to assess effectiveness must be clearly documented in the inception documentation. Any similar hedges must be assessed in a similar manner. Effectiveness testing is the quantitative or qualitative analysis that supports a company’s assertion that the executed derivative will be highly effective at offsetting the changes in fair value or cash flows of the underlying hedged transactions. A passing effectiveness test is required to apply hedge accounting.

Highly effective

ASC 815 limits hedge accounting to those qualifying relationships that are expected to be “highly effective” in achieving offsetting changes in fair value or cash flows attributable to the hedged risk during the period that the hedge is designated. In a quantitative assessment, highly effective is generally defined as a dollar offset or slope of the best fit line between .80 and 1.25, an r-squared greater than .80 and a F-table value of 4.129.

Collateral

Cash pledged to/from a dealer counterparty when the derivative is in a liability/asset position.

Cash flow hedge

A hedge of the exposure to variability in the cash flows of a recognized asset or liability, or of a forecasted transaction, that is attributable to a particular risk.

Missed forecast

To maintain cash flow hedge accounting, the originally documented hedged transactions must be highly probable (>80%) to occur. If no longer probable, hedge accounting should be discontinued and amounts previously stored in OCI should be reclassified immediately. An immediate reclassification is called a missed forecast and is documented separately in financial statement disclosures. A pattern of insufficient forecasting could impact future ability to designate hedges.

Fair value hedge

A hedge of the exposure to changes in the fair value of a recognized asset or liability, or of an unrecognized firm commitment, that are attributable to a particular risk.

Prepayment provision

A payment provision specifies a fixed or determinable settlement to be made if the underlying behaves in a specified manner.

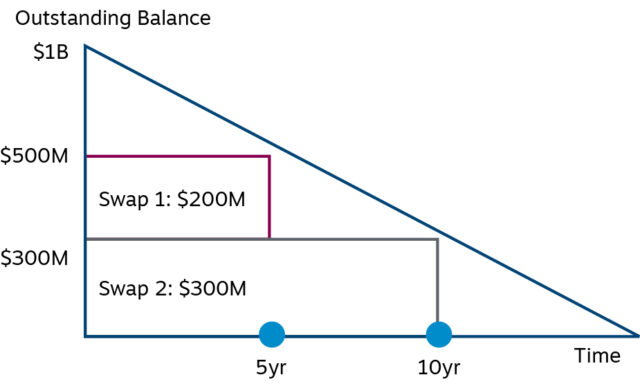

Portfolio layer method

One of the types of fair value hedge designations. For a closed portfolio of financial assets or one or more beneficial interests secured by a portfolio of financial instruments, the portfolio layer method allows an entity to hedge a stated amount of the asset or assets in the closed portfolio that is anticipated to be outstanding for the period hedged (that is, the hedged layer).

If the requirements for the portfolio layer method are met, prepayment risk is not incorporated into the measurement of the hedged layer. Multiple-layers within the same closed portfolio are permitted to be hedged with various hedging instruments including spot-starting or forward-starting bullet swaps, or spot-starting or forward-starting amortizing swaps.

Methodology

An example of portfolio layer method

Looking to learn more?

Contact a Chatham advisor today if you have questions.

About the author

-

![eri panoti headshot]()

Eri Panoti

Managing Director

Accounting AdvisoryFinancial Institutions | Kennett Square, PA

Eri Panoti leads the Financial Institutions Hedge Accounting practice and advises clients on hedge accounting policy and application for both balance sheet risk management strategies as well as customer hedging needs.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

22-0088