7 ways to maximize FX and commodity hedging impact while minimizing costs

-

Authors

Brittany Jervis

Managing Director

ChathamDirect and Hedge AccountingCorporates | Kennett Square, PA

-

Summary

Hedge program costs can range from forward points, to trading costs, to fixed and variable operational costs that include systems and personnel. Program benefits often include risk reduction, operational ease, and favorable accounting treatment. This article will address leading practices and current trends in maximizing the impact and return of hedging activities while minimizing costs.

After weathering massive, unexpected changes to consumer demand, supplier pricing, or foreign currency exposures, many treasury and accounting teams are either considering hedging for the first time or taking a step back to evaluate whether their existing programs still manage risk effectively and cost efficiently. The following seven steps provide a framework for maximizing the impact of your program while minimizing costs.

Maximizing impact amid a shifting landscape

1. Adjust for shifting organizational priorities

While you may review your operational hedging program every year, significant or unexpected market moves may require a more holistic assessment to ensure your strategic and tactical plan still addresses your risk sufficiently. Over time, and especially during periods of unexpected volatility, priorities can shift, creating a mismatch between your program and the objectives it aims to achieve. This means you may need to revisit fundamental risk management questions, such as, “Should we hedge risk?,” “How should we be hedging?,” and “Where does hedging fit in our organizational activities?” Internal triggers, such as missed forecasts, and external triggers, such as supply chain disruptions, can impact objectives, along with the strategies and tactics employed to achieve them.

2. Align all stakeholders and avoid silos

To capture all your risks and manage them appropriately, all stakeholders should communicate regularly and align on strategy. For FX programs, frequent interaction between front, middle, and back offices can ensure the economic strategy aligns with financial reporting. For example, an intentional over-hedging strategy allows for increased hedge volumes. However, the derivative notional is more than the amount of the underlying hedged transactions under this strategy, which makes it inappropriate for the Critical Terms Match (CTM) approach. While treasury may deem this strategy beneficial from an economic standpoint, your accounting team may need to put the proper documentation in place and gain auditor sign-off.

For commodities, this alignment becomes more complex since procurement or supply chain management, rather than treasury, is often tasked with managing this risk. By engaging with these stakeholders, you can collectively determine whether managing risks with derivatives might provide more control and flexibility than purchase contracts or supplier agreements. You can also avoid the risk of two functions operating at cross purposes, such as treasury executing a financial hedge while procurement executes a forward lock, which removes the risk and blows up the hedge accounting program. Additionally, when commodities contracts are priced in foreign currencies, it’s important to have awareness between treasury and procurement about the potential FX risk and alignment on how to manage that risk.

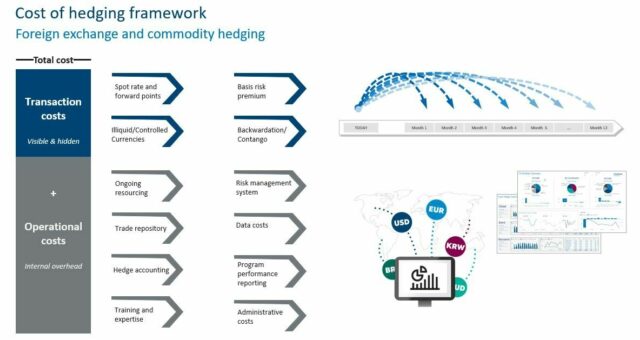

The cost of hedging framework

When assessing the costs of a hedging program, it’s important to define and quantify both the transactional and operational costs, which vary by the type of hedging program. Some will be fixed costs, and some will be more variable based on your actual trading volume. Because your strategic decisions can influence the costs you're paying, it’s important to perform a cost-benefit analysis and assess the tradeoffs stemming from different strategic choices.

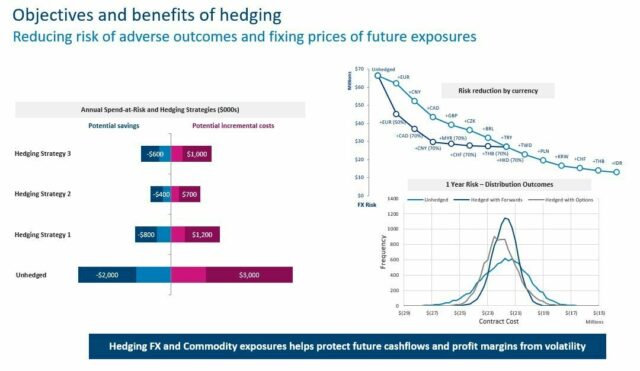

3. Define objectives and desired benefits

Companies primarily hedge so they can narrow the range of potential outcomes and create greater certainty.

- FX hedging can protect foreign revenues and expenses to protect profit margins, and can also limit volatility on your financial statements caused by balance sheet remeasurement.

- Commodity hedging can protect profit margins and financial statement volatility by fixing future prices for these exposures.

Beyond these high-level goals, however, financial risk management policies often rely on vague objectives, such as, “increase shareholder value” or “reduce risk at a reasonable cost” without including metrics to define success, input from stakeholders, or specific strategies and tactics to achieve each objective. It’s important to define how you will measure program costs against the benefits they provide. For example, many organizations may have deemed the Turkish lira or Brazilian real “too expensive to hedge” until their value fell by a huge percent. Specifically defining your risk/reward tolerance can help avoid inconsistent or subjective decisions when it comes to hedging.

Revisiting your goals and asking questions like, “Is our program still effective and doing what we want it to do?” or “Are we hedging the right currencies?” is a key starting point for identifying areas for change and improvement.

4. Define and quantify transactional costs

Ensuring an effective, compliant hedging program means assessing both visible and hidden costs across the spectrum of hedging activities, including strategy and pricing, legal and regulatory, and accounting. Once the full cost of the program is transparent, you can begin to identify the most cost-efficient mix of internal and external resources to support it. Quantifying transaction costs can be challenging because counterparties do not usually break out all the elements that make up a forward rate. Using a trading platform for FX hedging can bring more transparency and competition to the process if your company has a group of banks to trade against. It is also important to figure banking relationships into the equation. Are you willing to execute at a slightly larger cost to satisfy your banks? If so, how much more are you willing to pay?

5. Assess cost-benefit tradeoff strategies

Once you understand the components of your transaction costs, begin to consider the various levers you can pull to adjust cost-benefit ratios in your favor. Take a holistic approach and evaluate your overall risk profile. The relative impact of different strategic choices on cost-benefit tradeoff will vary based on your risk footprint and organizational objectives.

Choice of indices being hedged

For FX hedging, it often makes sense to reassess which currencies represent the highest risk to your organization and prioritize them for hedging. This can significantly reduce your risk profile without hedging every currency you’re exposed to. Understanding that you don’t need to reduce every risk to zero but rather narrow your band of outcomes to a manageable level, can provide both adequate risk protection and meaningful cost savings.

Other scenarios where you can identify and resolve inefficiencies might include:

- Your current selection of indices isn’t keeping up with your global expansion.

- You have a small exposure to a currency but it becomes highly volatile, raising the risk to your financials.

- You have natural offsets that you haven’t considered in your hedging program.

- Changes occur to the underlying commodity indices you’re exposed to based on procurement and contracting.

For commodity hedging, it’s important to inventory the commodities you’re exposed to within your supplier or customer contracts and determine the magnitude of each exposure. This includes reviewing the complexities and limitations of your supplier contracts. On the hedging side, this means reviewing your counterparty agreements and the indices which are liquid and available to trade on. With the financial, procurement, and supply chain teams working in tandem, you can make fact-based decisions, rather than knee-jerk reactions based on short-term price swings. Since many of these elements can change over time, it’s valuable to think holistically about your portfolio risk and which changes give you the most impactful results. For example, the commodity market is constantly evolving, and some commodities that may not have had a derivatives market a few years ago do now. Spending the time up front to analyze your exposures, make strategic hedging decisions, and plan for periodic reassessments, can deliver significant cost savings and program improvements.

Hedging tenor or horizon

Reviewing and adjusting the tenor and horizon of your hedges can enable you to adjust for a changing market environment and improve the cost-benefit equation. Some examples include:

- Trade layering: Instead of a static program where you add trades at one time for a 12-to-18-month horizon, you can add new trades quarterly or monthly, so you dynamically build a layered portfolio.

- Lower hedging threshold: Instead of hedging 80% of exposure, hedge 50% or 60% to build in more room for forecast uncertainty.

- Wider exposure window. Expand the exposure window from the default of one month to a three-to-six-month period, effectively borrowing hedging capacity from subsequent months. This strategy is enabled by a long-haul accounting strategy.

Choice of hedging product

Choosing which hedging instrument to deploy also presents cost-benefit tradeoffs based on the efficiency and simplicity of execution. On the operational FX side, Chatham sees about 90 percent of companies using a plain vanilla forward. This is a straightforward product that offers pricing efficiency and visibility, making the program easier to report on. However, if your underlying exposures are based on an average rate, you might want to consider a different product. If your objective is minimizing downside risk and protecting against an adverse move, you might consider executing options. With an option-based product, you lock in pricing and protect against your worst-case scenario.

This tradeoff also impacts commodities, where Chatham suggests a product selection that is informed by market data. For example, depending on prices in the market and volatility, companies may want to switch between swaps, collars, and calls to take advantage of the best pricing. Having a dynamic strategy allows you to be ready for market changes.

Basis risk

Basis risk, or the difference between your selected hedged index and the pricing index of the underlying physical exposure, can play a significant role in your cost-benefit calculation. In the below examples of the hedging index and product specification of the physical exposure, you could either view the charts as showing high correlation that sufficiently minimizes risk or deem the correlation too ineffective for hedging, depending on your objectives. Your cost-benefit analysis would weigh the directional benefit against the cost incurred to run the program. For commodities, where numerous potential indices offer varying degrees of liquidity, you should pay increased attention to whether the costs of hedging basis risk provide sufficient benefits. It’s also important to note that basis risk will introduce hedge accounting complexities that will likely require a long-haul approach to assess effectiveness, which is required to prove the program can qualify for preferential treatment.

6. Define and quantify the operational costs

Although forward points, option premiums, and other operational costs can be easier to see and quantify, your organization’s investments in people, systems, and work hours can represent a substantial portion of your program’s overall costs. Doing the work to quantify and manage these operational costs is a critical area for every treasury and accounting team to address.

Assess what your team can realistically manage

Many organizations have lean treasury teams, so operationally managing front-, middle-, and back-office processes should be part of the equation when determining how much of your risk to hedge. For example, can you afford to add two currencies to your program, including all the hedge accounting, journal entries, and reporting, or will this require adding an additional member to your team?

Treasury teams also struggle to hire people with the right skill sets, so key-person risk is a factor to consider as well. Hedging and hedge accounting are complex, niche areas within treasury and accounting. If only one person on your team understands how the program works, two weeks is not enough time to offboard a hedging program to a colleague. Although, Chatham subject matter experts can step in and help clients during these transitional periods, documenting your program and cross-training team members now can smooth the process and provide important safeguards in the case of unexpected employee transitions.

Employ technology to increase efficiency and control cost

Companies relying on a few people to manage treasury, or those managing their programs within spreadsheets, increasingly are converting to technology-based programs, where team members have defined roles within efficient, automated, controls-based processes. While integrating risk management technology with the broader technology stack was once challenging, new solutions enable easier movement of data from one set of tools to another, allowing for customization of processes and technology to maximize efficiency. From gathering and analyzing exposures, to executing and confirming trades, to settling trades and accounting for them, the risk management process includes numerous touchpoints where manual processes can introduce errors and delays. Understanding each of the functions in your treasury program, along with the multiple systems and processes that support them, such as enterprise resource planning (ERP) systems, trading portals, cash management platforms, and even spreadsheets and phone calls, serves as a first step in identifying processes that you can streamline and automate.

Many treasury teams have also incorporated business intelligence tools into their technology platform. Enhanced management reporting dashboards provide a concise, compelling overview of the economic and accounting implications of your program so you can make data-driven decisions and clearly communicate them to the senior leadership team, other business units, and the board of directors.

Subscribe to receive our market insights and webinar invites

7. Understand how commodities and FX costs impact financial statements

Whether or not you hedge financial risk, you should understand the impact of currency and commodity costs on your organization’s financial statements. For example, unless you apply hedge accounting, any gain or loss from the change in fair value of your hedges will be recorded directly to profit and loss on your financial statement. However, if your hedging strategies qualify for hedge accounting, those costs can be recorded in Other Comprehensive Income (OCI) until the hedged item affects earnings.

If you manage commodity pricing through supply-side contracts, you’ll see the cost reported in Cost of Goods Sold (COGS), which can cause significant fluctuations that may raise investor concerns. You should also conduct proforma assessments of your supplier contracts to determine whether they qualify as derivative instruments. Contracts to purchase or sell a fixed commodity amount should be evaluated to determine if the contract meets the definition of a derivative and, if so, whether it may qualify for the normal purchase, normal sales scope exception such that it doesn’t have to be carried at fair value with changes reported in earnings.

As companies face compressed margins due to rising commodity prices, treasury and accounting teams are increasingly looking to hedge and apply hedge accounting to exposures such as natural gas, steel, resin, and many other volatile markets. Because commodity hedging strategies may not perfectly match underlying exposures, understanding the nuances of hedge accounting can help minimize the volatility from these programs on your organization’s financial statements. This is especially important for organizations preparing for an IPO or otherwise expecting increased scrutiny.

If your organization seeks to apply hedge accounting, you will need to consider whether the critical terms match (CTM) or long-haul approach best fits your hedging strategy. While using CTM to qualitatively assert the program is effective can simplify your hedge accounting process, it is not appropriate for all strategies, such as the exposure window approach, intentional over-hedging strategy, or when basis risk is present. To avoid the risk of missed forecasts and support more dynamic programs, Chatham has seen many clients switch to long-haul with regressions. Often, this is supported by technology to ease the administrative burden.

From determining objectives through financial reporting, all the decisions you make come together in a way that can either enhance or detract from the effectiveness of your financial risk management program. As you consider each of the actionable levers for adjusting the cost-benefit equation, remember to also consider your program holistically, including efficiency, accuracy, pricing, and performance. With such a rapidly changing environment, staying nimble and accessing the necessary knowledge and tools to execute a successful hedging program has never been more critical. We look forward to supporting corporate treasury teams in the effort to manage financial risk efficiently and effectively.

Chatham Financial corporate treasury advisory

Chatham Financial partners with corporate treasury teams to develop and execute financial risk management strategies that align with organizational objectives. Our full range of services includes risk management strategy development, risk quantification, exposure management (interest rate, currency and commodity), outsourced execution, technology solutions, and hedge accounting. We work with treasury teams to develop, evaluate and enhance their risk management programs and to articulate the costs and benefits of strategic decisions.

Ready to talk about your hedging program?

Contact us to learn more about your hedging program's visible and hidden costs.

Disclaimers

Chatham Hedging Advisors, LLC (CHA) is a subsidiary of Chatham Financial Corp. and provides hedge advisory, accounting and execution services related to swap transactions in the United States. CHA is registered with the Commodity Futures Trading Commission (CFTC) as a commodity trading advisor and is a member of the National Futures Association (NFA); however, neither the CFTC nor the NFA have passed upon the merits of participating in any advisory services offered by CHA. For further information, please visit chathamfinancial.com/legal-notices.

Transactions in over-the-counter derivatives (or “swaps”) have significant risks, including, but not limited to, substantial risk of loss. You should consult your own business, legal, tax and accounting advisers with respect to proposed swap transaction and you should refrain from entering into any swap transaction unless you have fully understood the terms and risks of the transaction, including the extent of your potential risk of loss. This material has been prepared by a sales or trading employee or agent of Chatham Hedging Advisors and could be deemed a solicitation for entering into a derivatives transaction. This material is not a research report prepared by Chatham Hedging Advisors. If you are not an experienced user of the derivatives markets, capable of making independent trading decisions, then you should not rely solely on this communication in making trading decisions. All rights reserved.

22-0035